Grow Your

Wealth Without

The Confusion

Figure out how to generate the income you deserve.

Are You In Control Of Your Wealth?

Figure out how to generate the income you deserve.

Want To Earn More Money And Grow Your Wealth?

If you’re reading this, you probably have a decent job or small business of your own and an income that’s sitting just above the national average. But while you’re doing pretty well, you know you could be doing better. And you also know there are things you need to do so your money goes to the right places and starts to multiply on its own. So why aren’t you doing those things? It could be a mindset issue, a timing problem or simply the fact that you don’t know where to begin. As your personal wealth coach, this is where I come in.

What Does A Wealth Coach Do?

Most people think wealth is about money. As a wealth coach, however, I will help you expand your perspective on what is possible. We’ll help you articulate the life that you would like to live and highlight the things that have been getting in your way so that when we remove those things and replace them with habits, patterns and behaviors that will support you to live your wealthiest life, money flows from that.

My Services

Insight Session

Take the time to dive deep into your financial journey to date and the mental roadblocks which are holding you back from success.

Insight Session

Let’s talk about your goals and your mindset so we can make a plan for growing your wealth that works.

Insight Session

Want to generate more income? We’ll find out what’s holding you back before deciding how to move forward.

Financial Planning

Take care of the essentials before getting to the exciting plans which will grow your wealth for the long term.

Estate Planning

It won’t take long to make sure your family will have access to your assets if something happens to you.

Success Coaching

Work with me and let’s break down those barriers that are holding you back from really going for it.

Why Choose Nicky?

Years & Years Of Experience

I’ve been helping people take control of their wealth for thirty years.

Master Your Mindset

We all have set beliefs when it comes to wealth. We’ll work through yours to ensure they align with your vision.

Earn More!

Be even more promotable or take the leap into your own business by shifting beliefs and behavior that will potentially have you earning more.

Make The Right Decisions, Fast

Tired of wondering where to even start? Let me help you figure it out.

Take Action

With the team’s help, you’ll have assistance with keeping you on track of what’s the next action to prevent being overwhelmed on your journey to wealth.

Satisfaction Guaranteed

If you don’t think the coaching is brilliant in the first hour, I’ll refund your money, no questions asked.

Who I've Helped

Hear From Just A Handful Of My Happy Clients.

Let her guide you because it’s a wonderful experience.

- Wendy Horne

I came to see Nicky for a three hour Insight Session because I was just feeling really stuck with my money in the business like I wasn’t progressing. And out of the session, I’ve got clear goals of where to go next. I’ve got rid of some lifelong beliefs that just weren’t serving me at all . I’m really excited with the plans we’ve got in place to move forward. I will have a totally new concept of money and financially in place with my business. If you’re wondering whether the Insight Session is right for you, I would say absolutely go for it. You’re investing in moving forward. It’s definitely worth it. Don’t hesitate.

- Kimi Broadbent

Pilates Instructor

Nicky is there not to tell me what to do, But keep me in the direction I want to go in achieving my goals in my future. The return in investment is HUGE, I will be able to one day own a McDonald’s restaurant with confidence. I find that the more I’m challenged and the more I do it with Nicky, it’s just like training to run a marathon. You’ve got to keep doing it month after month, week after week to get it right. I’m comfortable with Nicky. It’s a person that I’m comfortable with that she will set me in the right direction. As our monthly coaching sessions are, things changed, and never the same. There’s always a new concern, a new issue or a new technique that I want to learn. Once you find that right coach, Why change?

- Chris Biden

McDonald's General Manager

Essential Insights

Tips and strategies to help you discover what’s possible when it comes to creating financial freedom.

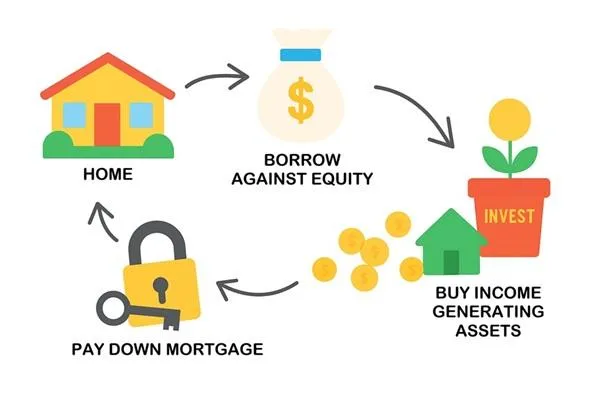

Debt Recycling Australia: A Guide to Build Wealth Faster

We’re all looking for smart ways to get ahead financially. One strategy you might hear about is debt recycling. It sounds complex, but the fundamental idea is quite simple: you turn your ‘bad’ debt into ‘good’ debt. Let’s break down what it is, how it works, and the things you need to watch out for.

What Is Debt Recycling?

At its core, debt recycling is a strategy where you systematically pay down your home loan (which is typically non-deductible debt) and then redraw those funds to invest in assets that have the potential to produce income, like shares or property.

The magic of this process is that the interest on the money you’ve redrawn for investing can become tax-deductible. This is because the Australian Taxation Office (ATO) generally allows you to claim a deduction for expenses incurred while earning assessable income. So, you’re effectively ‘recycling’ your home loan into a tax-friendly investment loan.

How Does It Work? A Step-by-Step Guide

The mechanics of debt recycling involve a few key steps. It’s vital to set this up correctly to keep your deductible and non-deductible debts separate.

Pay Down Your Home Loan:You start by making a principal payment into your home loan or offset account. For example, let’s say you make a $10,000 lump-sum payment.

Redraw the Funds:You then redraw that same amount ($10,000) from your loan. It is crucial that this redrawn amount is usedonlyfor investing.

Invest:You use the $10,000 to purchase income-producing assets, such as a portfolio of dividend-paying shares.

Claim the Deduction:The interest that accrues on that $10,000 portion of your loan is now generally tax-deductible. You must keep meticulous records to prove the funds were used for investment purposes. Tax savings and dividends can then be used to pay down your non-deductible home loan.

Over time, you can repeat this process, gradually converting your non-deductible home loan into a deductible investment loan and building a significant investment portfolio along the way.

The Main Benefits

Why go to all this trouble? There are two powerful advantages:

A Bigger Asset Base:You’re not just paying off a home loan; you’re simultaneously building an asset base in shares or property. This gives you two assets (your home and your portfolio) growing in value, rather than just one.

Tax Efficiency:By making some of your debt tax-deductible, you reduce your taxable income. This means you’ll pay less tax, freeing up more cash that you can use to pay down your home loan even faster or to reinvest.

A Simple Illustration

Here’s a simplified look at how the numbers might stack up. Imagine you have a $500,000 home loan and $20,000 in savings.

In the second scenario, while the total debt is higher initially, a portion of it is now working for you by funding an investment and providing a tax deduction.

What Are the Risks?

This strategy doesn’t come without risks, and it’s important to be aware of them.

Market Fluctuations:The value of your investments can go down as well as up. If your portfolio performs poorly, you could be left with a large debt and assets that are worth less than you paid for them.

Interest Rate Changes:If interest rates rise, the cost of your investment loan will increase, eating into your returns.

Records Management:Debt recycling requires careful management and good record-keeping. Mixing personal and investment funds can create a mess that’s difficult to sort out, especially with the tax office.

Is It Right for You?

You've seen how debt recycling can accelerate your wealth creation. Now, it's time to see how it can work for you.

Ready to turn theory into action? Book your call with a dedicated wealth coach now and start transforming your home loan into a powerful asset-building engine.

The Quick Guide To Unlocking Your Wealth

Ever Wondered How Some People Seem To Have Endless Amounts Of Money?

Find out in 9 simple steps.

So, How Do You Start?

Working With A Personal Wealth Coach Is Easy

The First Chat

In 15 minutes, we’ll talk about your goals, your current status and how I can help you walk a steady path to lasting financial freedom.

The Deep Dive

We’ll talk for three hours about your entire money story and identify the first steps you need to take (don’t worry, it will go FAST!)

Ongoing Service

Regular catch ups and introductions to all the right people will put the wheels in motion so you start seeing tangible results.

Yes, You Can Live a Wealthy Life

You have a coach for your fitness, why not have one for your wealth?

Get started with a free, no-obligation chat.

General Advice Warning

All strategies and information provided on this website are general advice only which does not take into consideration any of your personal circumstances. Please arrange an appointment to seek referral to the correct professional for financial, legal, tax or credit advice before acting on any information contained in this website. Nicky Stafford operates in Infinite Wealth Partners Pty Ltd. ABN: 76 635 869 644 Nothing on this site constitutes specific financial advice

© Nicky Stafford Business & Wealth Coaching 2025.